AN accountant, who is tasked with preparing the books of a corporate, will always be guided by accounting principles when it comes to how the financial statements of the company are presented on an annual basis to ensure they are accurate and reflective of the company’s business affairs. An auditor, looking at the same prepared accounts, will run through the numbers and audit the key material items to ensure they are reasonable, reflective of the company’s finances, and free from material misstatements, including due to fraud or error, or application of wrong accounting treatment. In financial statements, two of the most critical items are receivables and inventories. In order to have proper accounting treatment, accountants and auditors used accounting theories to describe what is deemed to be current, and those that have a longer-dated ageing profile are either impaired or written off. The reason for this is to ensure that the financial statements reflect the status of a corporation’s current assets and are in no way doubtful. There is also an application of general provision or specific provision when it comes to how these balances ought to be treated in the financial statements. Often, we see cases of over-inflated balances and when it came to the crunch of the matter, the management would have no choice but to write them off.

The ‘real’ overhang

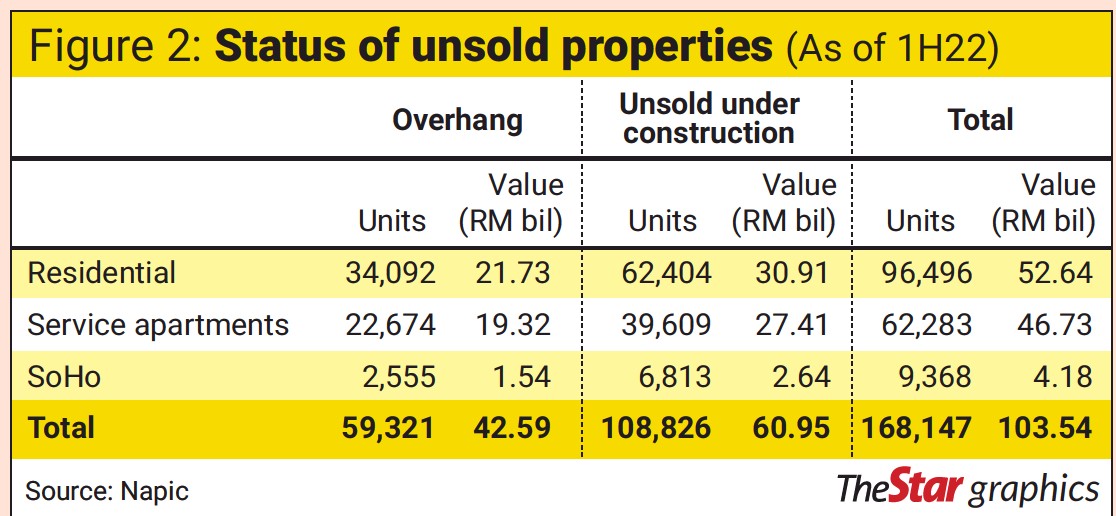

At the recently concluded 15th Malaysian Property Summit 2023, the Director of the National Property Information Centre (Napic) presented a paper on the status of the Malaysian property market up to the third quarter of last year (3Q22), with some data points related to the performance of the market up to November 2022. The full market report is only expected to be released in the middle of next month, where Napic will not only provide the usual annual update of the market’s performance but also provide more insight into some of the key data points that have been much discussed among all stakeholders, of which, one of them is the status of overhang in the market. As we are aware, the residential overhang at the end of 3Q22 stood at 29,535 units worth some Rm19.95bil. Napic’s website also provided the details of where these overhang properties are located and the three key states – Johor, Selangor, and Penang – are the main hotspots, accounting for some 14,956 units or just over half of the country’s total overhang. In terms of the type of properties, the 3Q22 data showed that high-rises comprise 18,962 units or 64.2% of the total overhang. In terms of price points, 23.8% of the total overhang was priced at RM300,000 and below, 29.5% was priced between RM300,001 and RM500,000, 31.6% was priced between RM500,001 and Rm1mil and the balance was priced above Rm1mil. In terms of the total value, the residential overhang is skewed towards the high-end segment with properties worth more than Rm1mil accounting for 43.4% of the total overhang value, while those priced between RM500,001 and Rm1mil accounted for 31.9% of the total overhang. Properties priced between RM301,000 and RM500,000 have a total overhang value of just Rm3.5bil, while properties priced below RM300,000 are worth some Rm1.39bil. These two represent some 24.8% of the total overhang value. For the service apartments, the total overhang in units stood at 23,688 worth some Rm20.21bil as at end of 3Q22, with Johor alone accounting for 62.4% of the total. Most of these overhangs in the segment are properties priced between RM500,001 and Rm1mil, which accounted for two-thirds of the total unit numbers and 58.9% in value of the total overhang. For the longest time, Napic had not shared with the stakeholders the key underlying ageing profile of this overhang, and that has led to a misleading status of the market’s overhang status. It was indeed an eye-opener to see what the real overhang has been. For example, as seen in Table 1, the key overhang is properties (both residential and service apartments across the four key states) that have been part of the statistics for the last five years and they account for between 51% and 93% of the total overhang units. For example, as seen in Table 1, the key overhang is properties (both residential and service apartments across the four key states) that have been part of the statistics for the last five years and they account for between 51% and 93% of the total overhang units. In total, these properties accounted for a whopping 75.7% of the market’s overhang status while properties that have been in the market for the last three years are just over 5% from the key states. Specific mention must also be made on service apartments located in Johor, and those that are in the five to 10 years bucket, as they account for 26% of the total market overhang. In terms of prices, most of the overhang is seen in the same five to 10 years bucket across the board and they alone account for 71% of the total overhang properties in the market. As seen in Table 2, properties below three years account for less than 5% of the total market overhang. Specific mention must also be made on service apartments that are in the RM500,001 to Rm1mil bracket and are in the five to 10 years bucket as they account for 25% of the total market overhang. In the corporate world, when one is up against data that is distorting the real picture, the proper thing to do is to see whether the data is still relevant or otherwise. Clearly, looking at the ageing profile of the property overhang, those above five years will likely remain unsold for a foreseeable future, mainly due to either being wrongly located and without the proper or good infrastructure to support community living, or untouched by property buyers for simply being too expensive, especially those beyond the RM500,000 price threshold. Clearly, looking at the ageing profile of the property overhang, those above five years will likely remain unsold for a foreseeable future, mainly due to either being wrongly located and without the proper or good infrastructure to support community living, or untouched by property buyers for simply being too expensive, especially those beyond the RM500,000 price threshold. Having identified the issues, regulators and property developers would need to come out with strategies to address them and to attract buyers to these properties via a rehabilitation exercise and with a significant price reduction. The bottom line is to remove them from the overhang data. Let’s call a spade a spade So what is Malaysia’s real overhang? Based on the data presented by Napic, one can take comfort that overhang is not as serious as it is made out to be mainly due to a lack of data and proper analysis in terms of what is real overhang previously. While those more than three years but less than five years are part of statistics, we should redefine them as core overhang while those beyond five years can be redefined as hardcore overhang. As we have been able to slice and dice these numbers, the real overhang is only perhaps less than 5% of the market in terms of the number of units and value. Napic could also help stakeholders to understand better the property market data better by breaking down the data points as an overhang that is mainly due to government housing schemes and those that are privately built. In this way, we could also see whether the government’s intervention is needed to boost demand for these obscurely located properties. For the private developers, most of these inventories would have been impaired as the likelihood of the assets being realised in full value or even at 50% to 60% of the market value is seen as low. Private developers too ought to think outside of the box on how to overcome the property inventories sitting in their books as being part of the statistics only results in painting the wrong picture for the property market as a whole.By Pankaj C. kumar is a long-time investment analyst. the views expressed here are the writer’s own.

Related posts: