src='https://pagead2.googlesyndication.com/pagead/js/adsbygoogle.js?client=ca-pub-2513966551258002'/>

Rightways: Silicon Valley Bank

Infolinks.com, 2618740 , RESELLER

It is crucial to improve the financial regulatory system and strictly maintain the bottom line of low risks, China’s former finance minister said at a forum on Saturday in commenting on the recent collapse of the US Silicon Valley Bank (SVB) that sent shockwaves across the US banking system.

The SVB bankruptcy suggests that financial markets have been hit by monetary policy changes, Lou Jiwei, director general of the Global Asset Management Forum and China’s former finance minister, said at the ongoing annual session of the forum, according to media reports.

The unconventional monetary and fiscal policies adopted by some countries during the COVID-19 pandemic have led to high leverage ratios across governments, households, enterprises, and financial institutions. These ratios rose quickly but would not fall easily, Lou said.

It has exacerbated the hikes of the inflation and its impact has been extended to the global financial market, with soaring volatility in stocks, bonds, foreign exchange markets, Lou said, noting that from a historical perspective, it may lead to a new round of crisis spilling over into emerging markets.

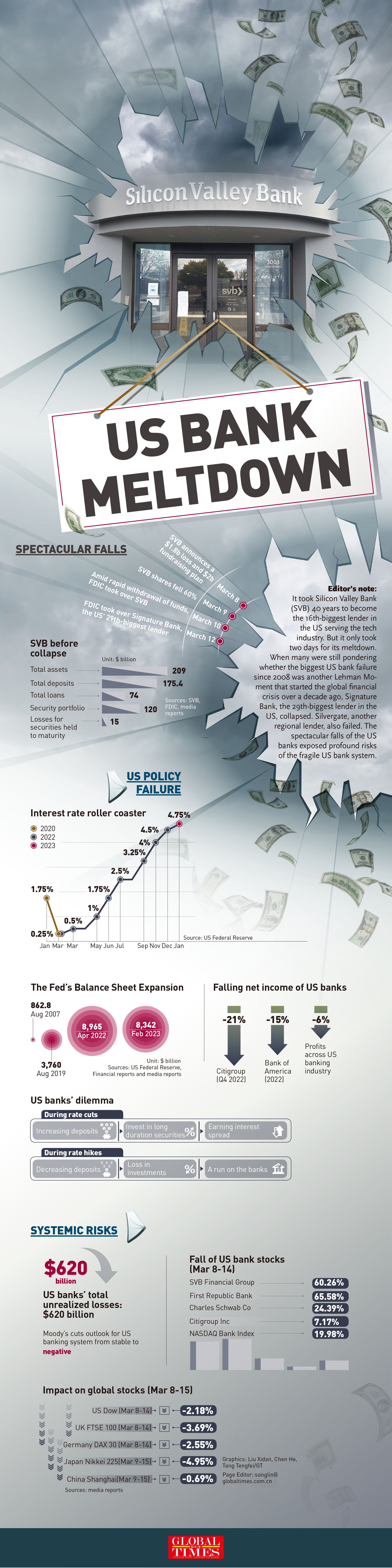

As the US 16th largest lender, SVB faced meltdown on March 10 after a 48-hour run on deposits. It marked the largest bank crash since the 2008 financial crisis. When many were still pondering whether it was another Lehman Moment that started the global financial crisis over a decade ago, the US 29th biggest lender Signature Bank closed by regulator just two days after the SVB collapse.

The unexpected bank failure has soon sent shockwaves across the US banking system, with jitters spreading across the global market.

NASDAQ Bank index, which contains securities of NASDAQ-listed banks, dropped 22 percent from 3981.59 on March 8 to 3100.16 on March 17. The First Republic Bank saw its share price plummeted from $115 to $23.03 during the period, down nearly 80 percent.

In Europe, alarms sounded at Credit Suisse, a 167-year-old Swiss bank which is also the 17th largest lender across Europe. Its share price has lost 30 percent since March 8. Although the bank secured a $54 billion loan from Swiss central bank to shore up its liquidity, its investor sentiment remains fragile.

The bank failure and emergency showed that the long-simmering profound financial risks in Europe and the US have reached a critical point of periodic outbreak, Dong Shaopeng, a senior research fellow at the Chongyang Institute for Financial Studies at Renmin University of China, told the Global Times on Saturday.

Banks are professional risk managers, and if they cannot manage risk effectively, then it means that the risk control system has failed, Dong said.

SVB is not the only risk point, a total of 186 US banks have reportedly been exposed to similar risks. “Even if only half of uninsured depositors decide to withdraw, almost 190 banks are at a potential risk of impairment to insured depositors, with potentially $300 billions of insured deposits at risk,” read an analysis conducted by New York-based Social Science Research Network.

Counting on its advantages as the world’s dominant financial power, US policymakers have believed that they could reap interests of others to plug their own loopholes. It is such “financial confidence” which has supported them to adopt a radical quantitative easing and then a drastic tapering policy, Dong said.

Yet, a considerable number of emerging countries are attaching more importance to financial risk management and firmly safeguarding their own autonomy, Dong said.

China has attached great importance to preventing and defusing systemic risks, and it is further improving its financial regulation including setting up a central commission for finance following the two sessions to optimize and adjust setting and functions of regulatory institutions, Lou said.

Lou said that China will continue to cooperate with other countries in financial regulation to jointly forestall and defuse systemic risks in the global financial system and maintain stability and prosperity of the global financial market.

The People’s Bank of China (PBC), the nation’s central bank, recently stressed the overall financial market is running smoothly and risks are under control. Large banks with excellent ratings are the “ballast stone” of China’s financial system. Reforms of a few problematic small and medium-sized financial institutions have achieved important progress, and illegal financial activities have been effectively curtailed, it said.

Amid a steep drop in the value of global banking shares following the SVB meltdown, however, Chinese banking shares rallied collectively. The Bank of China saw its share price surged from 3.33 yuan ($0.48) on March 8 to 3.48 yuan on March 17, reaching a five-year high.

The Chinese economy has contributed more than 30 percent of global growth annually for the past two decades, and this momentum will continue in the future, Yang Delong, chief economist at Shenzhen-based First Seafront Fund Management Co, told the Global Times on Saturday.

Under such circumstances, China’s strong enterprises, robust core assets will remain very attractive to foreign investment, Yang said, predicting that it is highly likely that the inflow to China’s A-share market from overseas investor will exceed 300 billion yuan this year.

Silicon Valley Bank was shut down on Friday morning by California regulators and was put in control of the U.S. Federal Deposit Insurance Corp..

In this photo illustration, Silvergate Capital Corporation

NEW YORK: Last Monday, the head of the Federal Deposit Insurance Corp (FDIC) warned a gathering of bankers in Washington about a US$620bil (RM2.8 trillion) risk lurking in the US financial system.

Last Friday, two banks had succumbed to it. Whether US regulators saw the dangers brewing early enough and took enough action before this week’s collapse of Silvergate Capital Corp and much larger SVB Financial Group is now teed up for a national debate.

SVB’s abrupt demise – the biggest in more than a decade – has left legions of Silicon Valley entrepreneurs in the lurch and livid.

In Washington, politicians are drawing up sides, with Biden administration officials expressing “full confidence” in regulators, even as some watchdogs race to review blueprints for handling past crises.

To his credit, FDIC chair Martin Gruenberg’s speech this week wasn’t the first time he expressed concern that banks’ balance sheets were freighted with low-interest bonds that had lost hundreds of billions of dollars in value amid the Federal Reserve’s rapid rate hikes.

That heightens the risk a bank might fail if withdrawals force it to sell those assets and realise losses.

But despite his concern, the toppling of two California lenders in the midst of a single workweek marked a stark contrast with the years after the 2008 financial crisis, when regulators including the FDIC tidily seized hundreds of failing banks, typically rolling up to their headquarters just after US trading closed on Fridays.

Even in the darkest moments of that era, authorities managed to intervene at Bear Stearns Cos and Lehman Brothers Holdings Inc. while markets were shut for the weekend.

In this case, watchdogs let cryptocurrency-friendly Silvergate limp into another workweek after it warned March 1 that mounting losses may undermine its viability. The bank ultimately said Wednesday it would shut down.

That same day, SVB signalled it needed to shore up its balance sheet, throwing fuel onto fears of a broader crisis.

A deposit run and the bank’s seizure followed. The KBW Bank Index of 24 big lenders suffered its worst week in three years, tumbling 16%.

“With Silvergate there was a little bit of a regulatory blind spot,” said Keith Noreika, who served as acting comptroller of the currency in 2017.

“Because they wound it down mid-week, everyone got a little spooked, thinking this is going to happen to others with similar funding mismatches.”

Representatives for the FDIC and Fed declined to comment.

The drama is already spurring arguments in Washington over the Dodd-Frank regulatory overhaul enacted after the 2008 crisis – as well as its partial rollback under President Donald Trump.

Trump eased oversight of small and regional lenders when he signed a far-reaching measure designed to lower their costs of complying with regulations.

A measure in May 2018 lifted the threshold for being considered systemically important – a label imposing requirements including annual stress testing – to US$250bil (RM1.1 trillion) in assets, up from US$50bil (RM226bil).

SVB had just crested US$50bi (RM226bil) at the time. By early 2022, it swelled to US$220bil (RM994.3bil), ultimately ranking as the 16th-largest US bank.

The lender achieved much of that meteoric growth by mopping up deposits from red-hot tech startups during the pandemic and plowing the money into debt securities in what turned out to be final stretch of rock-bottom rates.

As those ventures later burned through funding and drained their accounts, SVB racked up a US$1.8bil (RM8.1bil) after-tax loss for the first quarter, setting off panic.

“This is a real stress test for Dodd-Frank,” said Betsy Duke, a former Fed governor who later chaired Wells Fargo & Co’s board.

“How will the FDIC resolve the bank under Dodd-Frank requirements? Investors and depositors will be watching everything they do carefully and assessing their own risk of losing access to their funds.”

One thing that might help: SVB was required to have a “living will,” offering regulators a map for winding down operations.

“The confidential resolution plan is going to describe the potential buyers for the bank, the franchise components, the parts of the bank that are important to continue,” said Alexandra Barrage, a former senior FDIC official now at law firm Davis Wright Tremaine.

“Hopefully that resolution plan will aid the FDIC.”

The issues that upended both Silvergate and SVB, including their unusual concentration of deposits from certain types of clients, were “a perfect storm,” she said. That may limit how many other firms face trouble.

One complication is that the Fed has less room to help banks with liquidity, because it’s in the midst of trying to suck cash out of the financial system to fight inflation.

Another is that a generation of bankers and regulators at the helm weren’t in charge during the last period of steep interest-rate increases, raising the prospect they won’t anticipate developments as easily as their predecessors.

Indeed, even bank failures have been rare for a time. SVB’s was the first since 2020.

“We’re seeing the effects of decades of cheap money. Now we have rapidly rising rates,” said Noreika. “Banks haven’t had to worry about that in a long time.” — Bloomberg

Infographic: SVB meltdown exposes risks of fragile US bank system Infographic: GTSVB collapse highlights need to strictly maintain the bottom line of low risks

Infographic: SVB meltdown exposes risks of fragile US bank system Infographic: GTSVB collapse highlights need to strictly maintain the bottom line of low risks